AI Just Bought Me Lunch: Alibaba's Qwen Outruns Google in the Agentic Shopping Wars

You can now buy stuff directly in the LLM interface. Do order customization, payment authorization, and delivery coordination, without using any external platforms

I just ordered delivery directly through Qwen (Alibaba’s AI model), and honestly? I’m buzzing. I was so excited to share this, but my community’s reaction was surprisingly… muted.

Is it not a massive milestone that we can now handle the entire ordering process through an LLM? Think about it, it’s not just about food! You tell the AI your symptoms, and it selects and sends the right medication straight to your door (for the non-emergency stuff, obviously). That is a fundamental shift in how we live.

I was so pumped that I decided to write this article, which, for the record, is my first piece that has absolutely nothing to do with longevity or cryo.

While researching, I discovered that Google actually launched a similar capability a few weeks ago called the Universal Commerce Protocol (UCP). But why hasn’t anyone heard about it? It barely made a ripple in the West. Alibaba, on the other hand, didn’t just wait for people to get excited. They noticed the lack of enthusiasm and leaned in hard spending 3 billion RMB on “free delivery coupons.”

The result? Qwen is now the most downloaded AI app in China. It turns out that when you bridge the gap between “cool tech” and “free lunch” people finally pay attention (and the boba economy spiked - people placed over 10 million orders in 9 hours, surging to 120 million in 6 days)

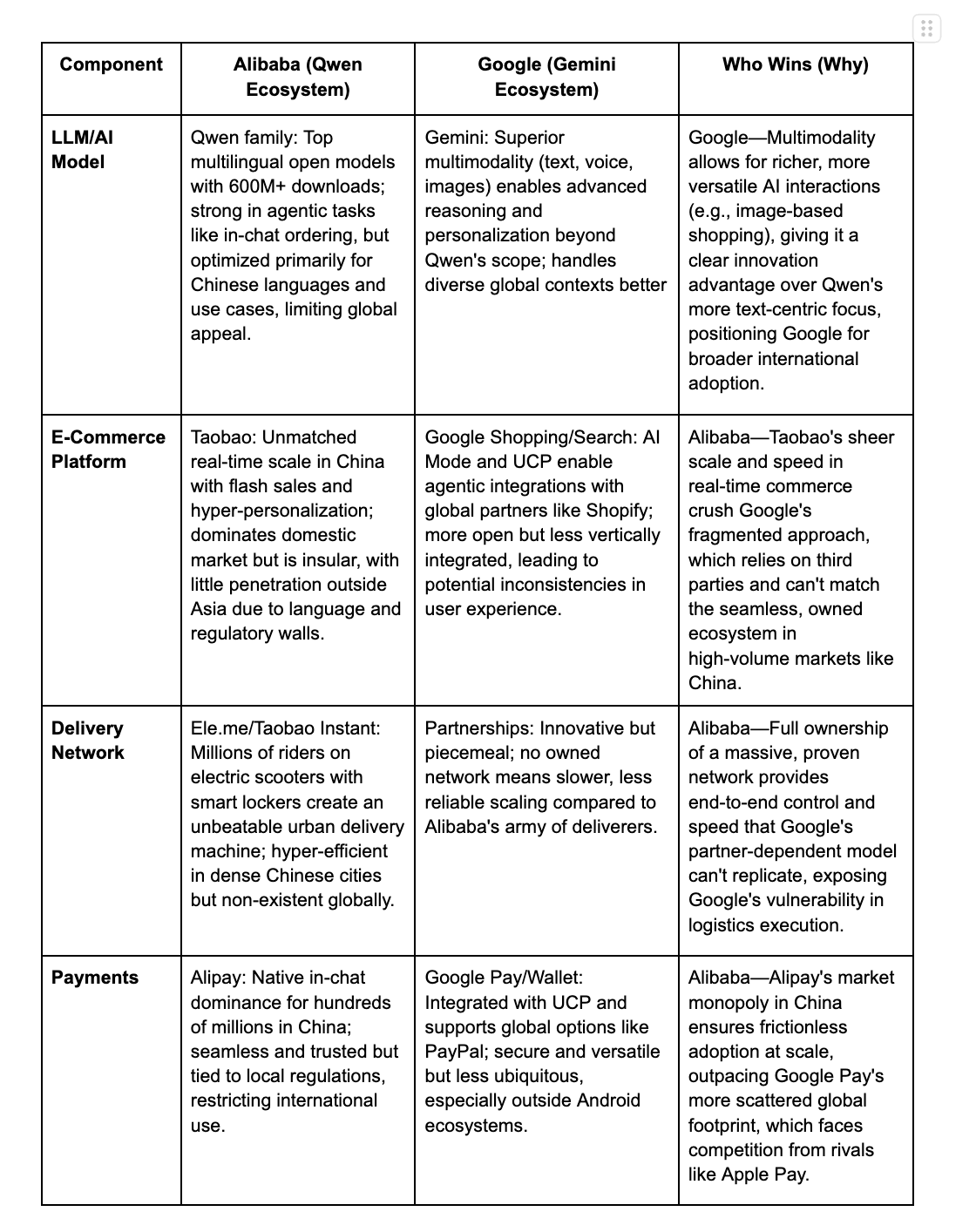

I decided to compare Google and Alibaba on their AI e-commerce startegy. Why not other companies? For e-commerce discussion, payment is a key discriminator. In the west, out of the 4 LLMs that matter (ChatGPT, Grok, Gemini and Claude), only Google has payment infrastructure (Google pay). In China, Alibaba and Tencent control the dominant payment rails, but only Alibaba aligns its LLM, commerce platform, delivery network, and Alipay into a single vertically integrated transaction stack.

Let’s try to understand what made it possible for Alibaba to such severly outcompete Google with basically the same e-commerce concept. It boils down to 4 categories: the LLM itself, shopping platform, payment and delivery.

Layer 1: The Intelligence Layer

At its core, the intelligence layer is about the raw capabilities of the AI models powering these systems: Alibaba’s Qwen versus Google’s Gemini. Both are cutting-edge LLMs, but their strengths diverge in ways that reflect their ecosystems and target markets.

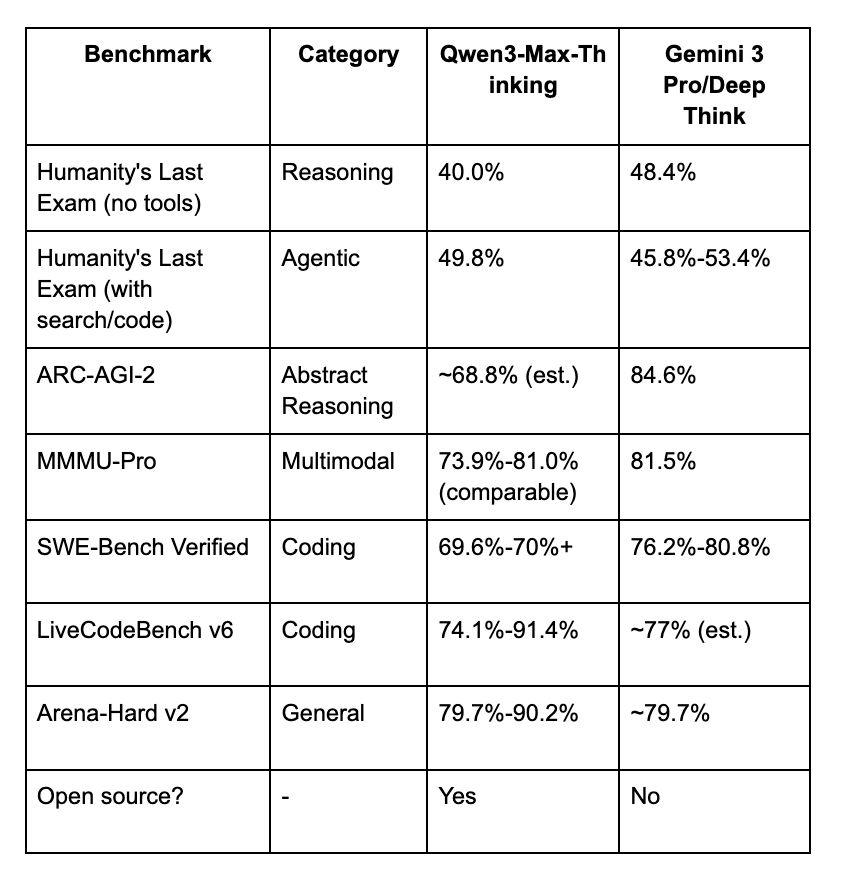

Gemini shines in global multimodality with seamless integration. It’s ranked highest on benchmarks like MMMU-Pro (multimodal understanding) and Video-MMMU, making it ideal for diverse, international applications where users might upload photos of ingredients for recipe suggestions or analyze videos for shopping recommendations. This broad capability stems from Google’s vast data resources, including YouTube and Search, allowing Gemini to process real-world inputs in a more “global” way. For instance, in agentic commerce, where AI acts on user intent, like booking or buying Gemini excels in long-horizon, multi-step workflows, such as planning a trip that involves parsing flight images, audio reviews, and code for integrations.

Qwen, on the other hand, is finely tuned for Chinese agentic tasks, emphasizing efficiency in multi-step reasoning and tool coordination within Alibaba’s closed ecosystem. It’s optimized for high-context scenarios common in China, like coordinating with local services (e.g., Ele.me for food, Amap for navigation). Benchmarks show Qwen3-Max-Thinking edging out Gemini 3 Pro on rigorous tests like Humanity’s Last Exam, highlighting its prowess in complex, agentic workflows requiring external data retrieval. Qwen’s hybrid reasoning supports custom agents for domain-specific tasks, such as e-commerce customization, without rigid structures.

But here’s the crux: Intelligence alone is inert without action. In China, Qwen wields “execution authority” through Alibaba’s vertical stack directly interfacing with Taobao, Ele.me, and Alipay to fulfill orders autonomously. Tell Qwen to “order a customized boba,” and it searches inventory, applies tweaks, processes payment, and dispatches a rider, all without leaving the chat.

In the West, Gemini operates in a fragmented landscape. Google’s UCP is an open standard, relying on partnerships with Shopify for e-commerce, Uber Eats for delivery, Stripe or PayPal for payments, and others. This means Gemini must negotiate permissions at every step: API calls to check stock, user consents for data sharing, compliance with local regulators (e.g., GDPR in Europe), and navigation through competing ecosystems like Apple Pay or Amazon. Fragmentation introduces latency and potential failures if a partner app glitches. As one analysis notes, while Gemini offers higher autonomy in reasoning, its agentic tasks often require more user guidance due to these external dependencies. The result? Agentic commerce feels constrained, like a powerful engine throttled by red tape. To truly compete, Google might need deeper integrations or acquisitions, but antitrust scrutiny could hinder that.

Layer 2: Commerce Density

China’s setup is a perfect storm for agentic AI: extreme urban density, scooter-based logistics, designated delivery cabinets, and the majority of households relying for delivery for everyday meals.

Average delivery times hover around 20-30 minutes, with costs per order low (around 18% of total payment, often subsidized). Abundant riders (estmiantes say about 10 million via platforms like Ele.me and Meituan combined). With China’s food delivery market at $40.2 billion in 2024, and 545 million users placing orders frequently, the ecosystem thrives on scale. We are moving from “Why would I take a 10 minute walk to a nearby shopping complex for a boba, if I can order it online?” to “Why would I bother opening an app and choosing the restaurant, and my order if I can just ask Qwen to do it for me while I take a bath/play my game/ work on my project*?”

Contrast this with the US: Suburban sprawl dominates, where homes are spread out, requiring car-based logistics that inflate costs (25% of order value) and times (often 45-60 minutes). Higher labor costs mean fewer riders per capita, and without widespread smart lockers, deliveries involve more handoffs. Consumers pay 30-40% more than the base food price via apps like DoorDash or Uber Eats, making it feel premium rather than routine. Usage reflects this: Americans order delivery about 4.5 times per month on average, versus China’s near-daily habit for many. App-switching friction compounds it; Gemini might suggest a meal, but you bounce to Uber Eats for checkout, killing the seamless agentic flow.

Also let’s not forget that Qwen food delivery is a huge win for people like me who take an hour to decide what do eat: “is it healthy?”, “but I had Thai yesterday…”, “I don’t feel like having chicken tonight”… Now, I can talk about it with AI and it can even suggest what would be healthier for me given my past food order history and biormakers (if I upload them;))

Layer 3: Payment

Alipay, launched by Alibaba in 2004, dominates China’s mobile payments landscape with over 1.43 billion users worldwide as of mid-2024, capturing around 54% of the third-party mobile payment market alongside WeChat Pay’s 40%. This duopoly accounts for over 94% of transactions, fueled by seamless QR code and biometric (face ID or PIN) payments that eliminate app-switching (try paying with cash in China, and DM me with how it went;)). In Qwen’s agentic setup, users confirm orders conversationally, and Alipay handles the rest—applying discounts, processing via stored credentials, and completing in seconds without leaving the chat. Low fees (often 0.1 yuan for small transfers) and no interest on wallets keep funds circulating within the ecosystem, boosting retention.

In Google’s UCP, payments integrate with Google Pay, using saved Wallet credentials for quick checkouts in AI Mode on Search and Gemini, with PayPal support incoming. However, this federated model introduces friction: reliance on third-party processors like Stripe or PayPal means variable fees (2-4% vs. China’s near-zero for in-ecosystem transfers), potential API latencies, and compliance with diverse regulations (e.g., GDPR, PCI DSS). Adoption lags, only about 25% of Americans use mobile wallets like Google Pay, compared to China’s 73%+ for daily transactions. Cultural factors compound this: U.S. consumers prefer credit cards for rewards and protections, leading to slower shifts from traditional methods.

What’s next?

Naturally, right after the initial wonder of my first LLM purchase, I started having questions and concerns. Thankfully, it’s still a human-in-the-loop system, so AI can’t just go rogue and buy stuff with your money that it deems beneficial. The next big worry? Ads. If the cognitive load of switching platforms and fumbling through payments gets wiped out, you could just tap an ad and buy on impulse, especially when it’s hyper-targeted, with the AI knowing your emotions, health status, and financial situation. Any illusion of independent thinking while shopping? Trashed. Also, will this further exacerbate the problems baked into the platform economy, if your shop (at least in China) isn’t hooked into delivery networks, you basically don’t exist (though the case is nuanced, ofc). These AIs train on skewed data, potentially funneling you toward Alibaba-favored brands or culturally dominant options, quietly marginalizing less tech oriented sellers (this tips hard into our Right to Be Remembered paper).

And then there is a case of privacy. Qwen already taps into my order history and could soon pull biomarkers or mood data from wearables, handing Alibaba (or hackers) a god’s-eye view of my life.

There are questions, there are simulations, there is a ton of scenarious.

But for now… hey Qwen, can you get me a big cup of the duck poop hand beaten lemon ice tea, no sugar, less ice?

iykyk